There is a lot of focus on the UK aviation restart at the moment particularly when it comes to the climate change aspects. Commentators from across industries have been encouraging the Government to make the restart green and to seize the opportunity presented to rebuild carbon-intensive industries such as aviation in a more sustainable fashion or to ‘Build Back Better!’.

It is therefore timely that the Government have reported on their plans for a UK Emissions Trading Scheme (UK ETS), which pending further Brexit shenanigans will come into force in January 2021 to replace our current participation in the EU scheme.

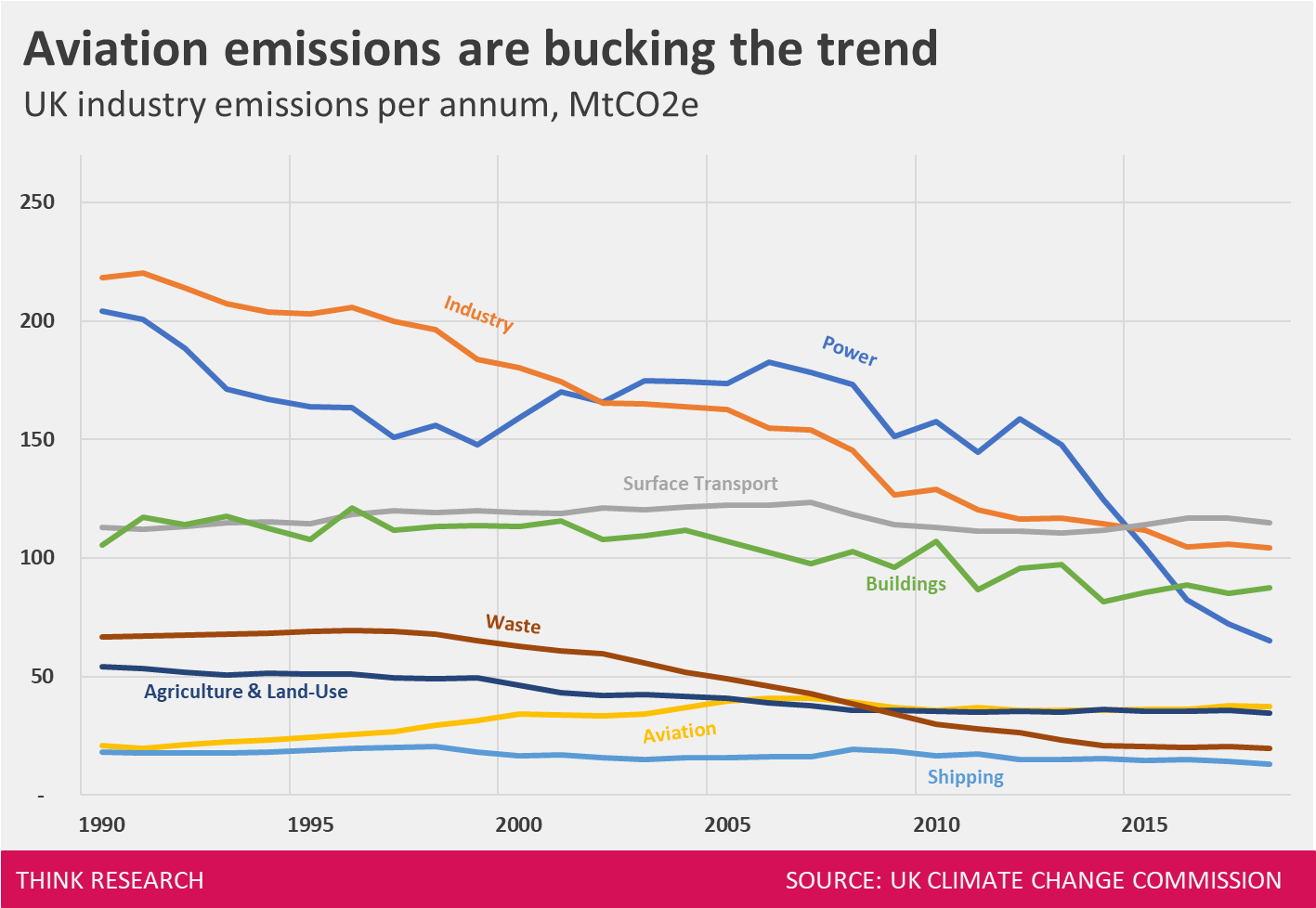

Where are we as an industry?

It is worth appraising where the aviation industry in the UK is with respect to emissions as often statements in the press are made based upon data from global or EU aviation.

The UK’s greenhouse gas (GHG) emissions are around 1% of global emissions, approximately the same as its share of global population. In their July 2019 report to Government, the UK Climate Change Committee (UKCCC) reported that UK GHG emissions fell by 2.3% in 2018 to 491 MtCO₂e and have fallen 40% since 1990. Aviation emissions data lags by a year so for 2017, total aviation emissions increased by 3.5% to 36.5 MtCO₂e. Emissions from international flights increased by 3.6% to 35.0 Mt and emissions from domestic flights increased by 2.6% to 1.5 Mt. Overall, emissions from aviation in 2017 were more than double 1990 levels. Clearly, in this time there has been significant passenger and movement growth, so emissions per passenger has declined. It is fair to say that for an industry that receives such negative press on our sectoral emissions we are far from being the worst offender. Nevertheless, as the figure below shows, UK aviation’s emissions are steadfastly bucking an otherwise (mostly) good trend.

The UKCCC proposed a net-zero GHG emissions target for the UK for 2050. It should be remembered that even if this target is achieved globally, it is still highly likely to give rise to 1.5 degree C temperature rise. Under this plan expected actual emissions would reduce by 80% from 1990 levels by 2050 with remaining emissions then offset or captured. Aviation reductions have been accepted as not being fully possible in the 2050 timeframe and it has been assumed that they will be no higher than 37.5 Mt in 2050. If all other sectors de-carbonise as planned then that would see aviation representing around 25% of all UK emissions in 2050, a substantial increase in share. In part this is one of the key reasons for the concern around aviation’s emissions [1].

From the industry side, the Sustainable Aviation group of UK airlines, airports and NATS have outlined a roadmap for the industry to reach net-zero emissions by 2050. The plan is predicated on delivering a 70% increase in passenger volumes in the same timeframe. You can have a look and play with a chart summarising the year by year emissions here.

Hmmm. Massive passenger growth and net-zero emissions. Almost sounds too good to be true…

What’s wrong with that roadmap chart? Cursory review of the roadmap highlights a number of issues such as the assumption of additional runway capacity in the UK around 2026, a growth in absolute emissions through 2035 (oh great, bad PR for the next 15 years…), a sudden uptick in sustainable fuel use suspiciously close to 2050 and assumptions about new generation fleet performance. All of this is underpinned by an assumption of the quality of offsetting measures required to achieve the net position.

Nevertheless, all faults aside, the industry objective is better than regulation alone would require, resulting (if achieved) in emissions of 25.8Mt in 2050 versus a UKCCC assumption of 37.5Mt.

The airlines themselves have been considering their position in light of much of the negative publicity received. IAG for example has a ‘Flightpath net zero’ project which aligns to the 2050 net zero target of Sustainable Aviation delivered on the basis of on-going improvements in emissions per passenger although noting again this provides the opportunity for absolute emissions to rise. EasyJet have started offsetting their emissions across their network. Ryanair have set some 2030 targets on emissions per passenger, but no limits on total or net emissions.

All airline and industry plans and indeed the Government’s expectation is that offsetting and emissions trading will remain essential for the UK aviation industry through to 2050. Which brings us to the detail of the scheme proposed.

UK Emissions Trading Scheme

The principal of an ETS is that a cap on the total emissions allowed by carbon-intensive industries covered by the scheme is set. Allowances that add up to the cap are provided to companies within the regulated industries. These companies are required to measure and report their carbon emissions and to exchange one allowance for each tonne they release. Companies can trade their allowances between them, providing an incentive for them to reduce their emissions but also effectively providing a licence to pollute for those who cannot curtail their emissions.

The Governments approach to the UK ETS has been largely based upon the plan for Phase 4 of the EU ETS, which the UK had been heavily involved in crafting. However, in a positive move, the Government has chosen to go further than the EU ETS, aiming to reduce the existing emissions cap by five percent. The Government has committed to investigating close alignment to the EU ETS scheme such that credits accrued in each scheme could be used between the systems, but right now that is just a desire. Aviation is still within scope and the UK ETS will govern:

-

-

- Domestic flights in the UK.

- Flights from the UK to EEA States.

- Flights from the UK to Switzerland (pending agreements with the Swiss Govt.).

- Flights between UK and Gibraltar[2].

-

There are size limits on the type of aircraft that are included (<5700kg excluded) and a lower level flight movements threshold below which operators with limited flight movements are also excluded. Some business jet operations will therefore likely be excluded due to the lower usage by smaller operators.

Interestingly, there will be targeted reviews of the free allocation of credits to aviation and further consideration of how to integrate the scheme with ICAO’s global market-based measure the Carbon-Offsetting and Reduction Scheme for International Aviation (CORSIA). The Government have stated that the UK ETS is likely to augment CORSIA which is similar to current thinking within the EU. There will also be further assessment of a possible Carbon Emission Tax as an alternative to the UK ETS, but we won’t hear more about that until later this year.

Overall, the UK’s proposed scheme is therefore of little surprise to the industry and the changes compared to the EU scheme are somewhat minimal at face value. Nevertheless, between free credits allocated to aviation, exclusions for certain locations/operators and the need to reconcile the scheme with CORSIA it is clear that this is part of a work in progress in terms of our industry’s emissions.

Our own greatest enemies?

It is true that as an industry we haven’t helped ourselves when it comes to climate matters. We were late to the game in terms of understanding the public mood around the climate and have not helped ourselves with some of the measures we have put in place. More recently, much of the European airline industry has accepted Government loans or bail-outs largely free of any environmental constraints and despite many making large dividend payouts only months earlier when COVID was known about.

If you look at the positions taken by certain industry trade bodies the impression that you may form is of an industry that wants to have its cake and eat it. Strict emissions reductions have been kicked down the road to 2050, carbon-neutral growth from 2020 is proposed but without a mechanism to enable it and all targets are net of offsets. Now clearly, such organisations sit as far on one end of the spectrum of balance as the environmental NGOs who hate aviation sit on the other, but nevertheless such positions hurt us more than benefit us.

Well-meaning airlines have proposed (or are) including offsets in the ticket price for flights, but offsetting is an area fraught with challenges in terms of price, quality, whether the offsets would happen anyway, etc.

(Insert chosen expletive here) CORSIA

Perhaps the most concerning position the industry has taken is over the oft-repeated claim that the ICAO CORSIA scheme will provide the answer to curtailing aviation’s environmental impact. It is logical to suggest that in an international business the environmental response too must be global to avoid competitive distortions and leakage of emissions. Unfortunately, the reality is that CORSIA is an unambitious, weak scheme, currently unfit for the climate challenge the world is facing. The scheme is still largely voluntary for a few years yet (the burgeoning Chinese aviation market is not yet included for example), is largely offset based with continuing uncertainty over the quality of the offsets and is unlikely to be compatible with the Paris climate agreement goals[3].

Having worked in the international standardisation environment it is understandable how the scheme developed as it did. ICAO is part of the UN and approval of international standards requires agreement amongst Member States, many of whom have an interest in continued expansion of aviation without concern for the environment or on the assumption someone else will pick up the bill. However, the greatest sin is not the scheme itself, it is those who in full knowledge of its weaknesses claim that it is the answer. It is not, and it weakens our case as an industry. It is no surprise that the EU and UK view it as necessitating additional measures to contain aviation’s emissions.

Whilst it has to remain a priority to sort CORSIA out so that it has a much greater level of ambition and coverage we also have to acknowledge such actions in ICAO are State level and therefore in the realm of international politics. However, what we can do as an industry is:

1. To stop hiding behind CORSIA as being the answer until it is properly reconciled with the Paris agreement;

2. Press and lobby States to advance the ambition and early involvement of all States in CORSIA at ICAO level. One mechanism to achieve this might be to use the impact of COVID on aviation to set a lower sectoral emissions baseline;

3. Accept that regional market mechanisms are, in places, currently more credible than CORSIA for long-haul inclusion and that they may be the pragmatic way forward for the industry despite all of the distortionary competition impacts they bring.

Also, those organisations presently lobbying ICAO to use COVID as an opportunity to reduce the cost of CORSIA on the industry should seriously consider whether they are going to be on the right side of history here. Not great PR if their European airline member’s passengers were to find out…

A greater level of ambition

There are many outside our industry currently capitalising on our (necessary) internal focus to promote their agenda of shutting down aviation and suggesting all sorts of restrictive measures largely unchallenged and without any consideration of the benefits of aviation. We as an industry need to get back into the debate before any chance of a recovery, green or otherwise, is throttled.

Talking with colleagues from across the industry, both before and since the COVID collapse, it is apparent that there is a good level of support for our industry being more ambitious in its climate objectives. The vast majority of people working in our industry do not view it as an act of cognitive dissonance to be strong supporters of climate action whilst also wanting to preserve the benefits of international aviation. For every industry climate denier who wants unfettered growth and for the planet to burn there are thousands of people who see reduced growth, living within a carbon budget and heavy investment in new technologies as eminently sensible and desirable.

There are a number of things that can be done at the UK level that are meaningful and not just tinkering at the edges[4] of the climate challenge, e.g.:

1. Actively identify and promote credible alternate solutions for short-haul travel. In many cases, air travel over relatively short haul distances can easily be substituted by high-speed rail travel or in the near-future by emerging urban air mobility solutions. Airlines (and airports for that matter) should identify and market such opportunities to travellers as a substitute for flights. A good recent example being the KLM Air&Rail product whereby flights from AMS to BRU are being reduced with capacity on the Thalys being used instead. We’ve seen similar things before from London to Brussels and elsewhere[5].

2. Let’s sort out the UK airspace with a focus on carbon. We’re in the midst of a national level Airspace Modernisation Programme. We should be seizing the opportunity afforded by the downturn to push the reorganisation through as fast as possible to give us the most efficient airspace design possible. Part of that has to include the Government taking another look at the balance of priorities for noise versus carbon in that redesign.

3. Let’s get a clear industry position on the quality of offsets to be used where absolutely necessary and hold ourselves to the highest possible standard. In the interim, airlines can hold competitors to account on their offset standards and lobby for independent carbon audits.

4. Agreeing collective targets for the use of sustainable synthetic/bio-fuels to help create the market for those products and to invest to ensure they are delivered in line with the recommendations to Government from Sustainable Aviation. It has been positive to see movements in this direction in recent days from the UK Government from their Jet Zero Council.

5. Industry level target setting and reporting, e.g. through Sustainable Aviation, to show how our collective efforts are achieving progress and how we as an industry are playing a full part in reducing our impacts. Let us take the Sustainable Aviation Roadmap to Net Zero as a starting point and correct for some of the out of date assumptions, e.g.:

-

-

- New runway capacity in the South East is looking increasingly unlikely. Remove the planned traffic growth as a consequence of that and re-baseline the traffic assumptions on the basis of the COVID impacts.

- COVID has led many airlines to park or decommission older aircraft. Consider advancing the assumptions about the mix of fuel-efficient modern types in accordance with current industry planning.

- See what is feasible in terms of expediting ATM efficiencies whilst traffic levels are lower (see 2 above and 6 below).

- Aim to produce a plan that does not see gross emissions increase above 2019 levels, ideally targeting at least a linear reduction to the 2050 end state from 2019 onwards.

-

6. The ATM sector and airports should consider continuing to invest in new technologies that would boost capacity (e.g. Time Based Separation, AMAN/DMAN integration, etc.) but use the capacity created to remove holding delays and thereby minimising airline carbon emissions.

We must also be honest, about our impacts, the credibility of our solutions and in accepting that there will be capping of demand until the link between flying and carbon can be broken. But if ever there was a time to accept that impact, it is now.

Summary

It has been a torrid year for our industry, and it is not over yet. The impacts have been devastating and many great colleagues in airports and airlines have lost their livelihood. However, whilst we have been battling to survive the climate emergency has not gone away, and the critics of our industry have been revelling in bad PR from the bailouts and loans we have taken largely free of environmental restrictions. We also have not always acted in a responsible fashion when it comes to the climate.

At the same time, people want and, in many cases, need to fly. The benefits of aviation are oft-overlooked in the climate debate. Long-haul flying provides people with experiences they could never have in the UK, the opportunity to learn about new cultures and broaden their outlook. It connects families in our globalised world, gives business access to new markets and customers and allows business and academia to work internationally.

Aviation, whilst being the focus of much of the environmental NGO’s focus is only part of the problem, and still a relatively small part at that. There is scope for the industry to further improve, to allow us to meet Paris agreement objectives and preserve the ability of people to travel. Yes, let us think more carefully about our impact before jetting off and sure, make best use of Zoom or Teams to save on unnecessary travel. However, where new relationships need to be built, where there is a need to win new work and build trust there is no substitute for face to face meetings.

It is timely for a more conciliatory approach to environmental concerns. We need to be honest about the carbon-intensive nature of flying, to be our own harshest environmental critics and to set the great talent and resources available to our industry to do everything we can to limit our impacts, and yes – even if this means suppressing demand. But equally, we need to protect the upside of travel and be willing to speak up for our passengers.

Author: Steve Leighton, Airports Director

Additional Notes

[1] Whilst this is the focus of much concern, and setting aside the obvious concerns about the ability of other sectors to decarbonise internationally, the focus on this 2050 figure should be subject to scrutiny. There are 30 years of each industry’s cumulative emissions to consider before we reach 2050. This rather overshadows the 2050 end state alone and prompts further questions about the apparent focus on aviation as the great climate killer. However, we’ll leave that point aside for now.

[2] Interestingly, flights to/from the Isle of Man, Jersey and Guernsey are excluded as are popular destinations in the EU Outermost Regions such as Madeira, the Azores and the Canary Islands.

[3] Although ironically, the scheme baseline (at least in the pilot phase) was planned to account for the sectoral emissions average across 2019 and 2020, IATA have lobbied to change that https://carbonmarketwatch.org/publications/carbon-market-stakeholder-letter-to-icao-council/.

[4] Happy as we are to see Air Traffic Management (ATM) taking the climate challenge seriously in the EU they only influence around 6% of emissions and horizontal flight efficiency is in excess of 97%. Similarly, it is great that many UK and EU airports are on track to be carbon neutral, but again an airport’s activities are small fry when viewed against flight emissions.

[5] It still surprises that we have e.g. London to Manchester and London to Newcastle flight services when the train times are competitive. Whilst many would say that is due to untaxed aviation being too affordable, there are clearly also aspects of the broken UK rail franchising model and lack of investment that leads to prohibitive peak time ticket prices for business travellers combined with overcrowding. It should also be noted that in the short term a large scale shift from aviation to rail is unlikely to be able to be accommodated easily – HS2 anyone?

Recent Comments